Fed Rate Cut 2025 Impact on Mortgage Rates and Housing

Lisa Mailhot | December 10, 2025

Buyers

Lisa Mailhot | December 10, 2025

Buyers

Disclaimer: This blog is for informational purposes only and may reference third-party sources, including quotes or data used verbatim with proper credit. All efforts are made to ensure originality and avoid plagiarism. Readers should verify details independently and consult a licensed professional before making real estate decisions.

The Federal Reserve just made headlines again with its third consecutive interest rate cut of 2025, bringing the benchmark federal funds rate down to a range of 3.5% to 3.75%. As the owner of Whitestone Real Estate and someone who's been navigating the real estate market for years, I can tell you this decision has everyone talking—from first-time homebuyers to seasoned investors across the country.

But here's what caught my attention. While the Fed delivered this quarter-point cut as expected, their projections for 2026 tell a very different story. And that's what I want to unpack with you today, because understanding this shift could dramatically impact your real estate decisions in the coming year.

This Wednesday's rate cut marks a significant milestone—the federal funds rate is now at its lowest point since November 2022. We've seen the Fed slash rates by three-quarters of a point since September, moving steadily to combat economic headwinds and support a softening job market.

However, this wasn't a unanimous decision. The Federal Open Market Committee was more divided than it's been in six years, with three dissenting votes. Two members wanted to pause cuts entirely, while another pushed for a more aggressive half-point reduction. Fed Chair Jerome Powell himself admitted it was "a close call," and that he "could make a case for either side."

What does this division tell us? The Fed is walking a tightrope between supporting the labor market and managing inflation that remains stubbornly above their 2% target.

Here's where things get interesting for homebuyers and sellers nationwide. While the Fed cut rates today, their updated economic projections reveal they're expecting just one additional quarter-point cut throughout all of 2026.

Let me repeat that. One cut. Next year. Total.

This is significantly less aggressive than what many market participants were hoping for. Some traders had been pricing in two or three cuts for 2026, so this projection represents a reality check for anyone expecting rates to keep tumbling.

The Fed's optimism about economic growth is actually driving this caution. They're forecasting GDP growth of 2.3% in 2026, up from 1.7% in 2025, while expecting inflation to cool to 2.4% by the end of next year. Translation? They believe the economy can handle higher rates for longer.

Now, let's talk about what really matters to you as a homebuyer or seller—mortgage rates.

First, a crucial point that many people misunderstand. Mortgage rates don't move in perfect lockstep with the Fed's benchmark rate. The federal funds rate primarily influences short-term borrowing costs like credit cards, HELOCs, and adjustable-rate mortgages. Your typical 30-year fixed mortgage? That's tied more closely to the 10-year Treasury yield and broader investor sentiment.

As of today, the average 30-year fixed mortgage rate sits around 6.26% to 6.35%, depending on your source and qualifications. That's actually down from the eye-watering highs we saw in late 2023, when rates briefly touched above 8%. A borrower taking out a $500,000 mortgage today would save roughly $584 per month compared to those peak rates—that's real money back in your pocket.

But here's the nuance. Mortgage rates often anticipate Fed moves rather than react to them. We've seen this pattern repeatedly in 2025. In both September and October, mortgage rates actually fell to multi-year lows right before the Fed announced their cuts, not afterward. In some cases, rates even ticked up slightly in the weeks following the official announcement.

Why? Because lenders price in these widely expected moves ahead of time. By the time the Fed makes it official, the market has already adjusted.

If you're looking to buy a home, here's my advice based on decades of experience in this market.

Don't try to time the market perfectly. I've watched countless buyers sit on the sidelines waiting for the "perfect" rate, only to see home prices appreciate faster than rates declined. Remember, you marry the home but date the rate—you can always refinance later if rates drop significantly. What you can't do is recapture the home you missed out on.

The Fed's projection of limited cuts in 2026 suggests that anyone waiting for rates to plunge back to 4% or 5% might be disappointed. With the economy showing resilience and inflation still above target, those rock-bottom pandemic-era rates look increasingly like a historical anomaly rather than a baseline we'll return to soon.

Shop aggressively for your mortgage. In today's environment, different lenders can quote rates that vary by a quarter to a half percentage point or more. That difference on a $500,000 home could mean tens of thousands of dollars over the life of your loan. I always tell my clients to get quotes from at least three to five lenders including a big bank, a credit union, a local mortgage broker, and a couple of online lenders.

Consider alternative loan products too. While the traditional 30-year fixed mortgage is America's favorite, it's not always the best choice. Adjustable-rate mortgages typically offer lower initial rates than fixed-rate loans. If you plan to move or refinance within five to seven years—which many buyers do as they trade up—a 5/1 or 7/1 ARM could save you significant money.

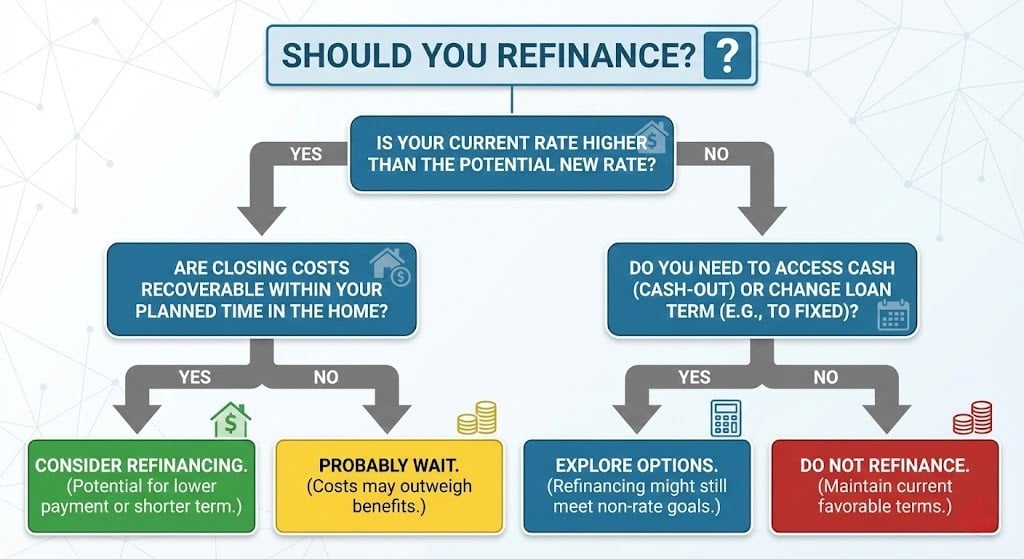

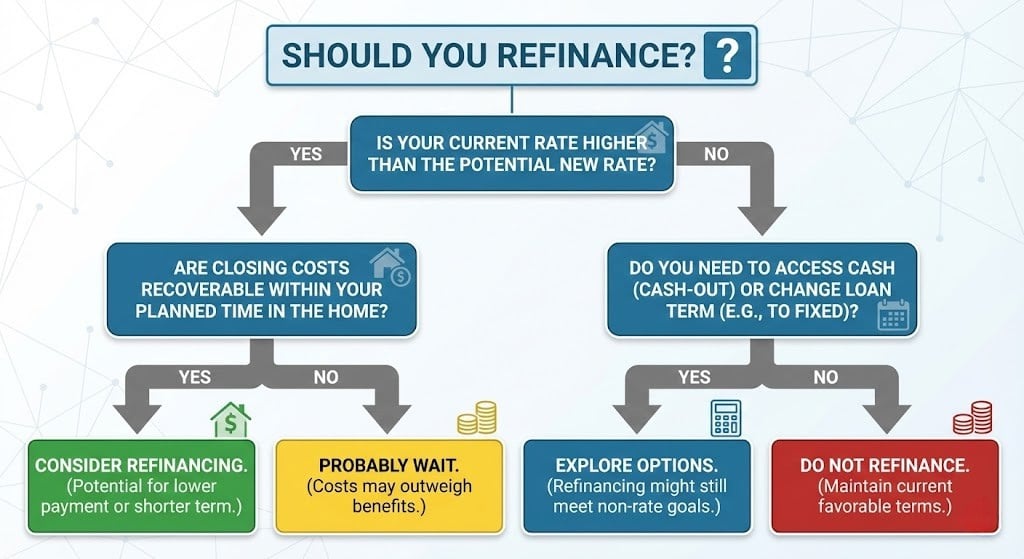

For current homeowners, the refinancing calculus remains tricky. If you locked in a rate below 4% during the pandemic years, there's virtually no scenario where refinancing makes sense right now. Your rate is gold—protect it at all costs.

However, if you're sitting on a rate above 7% from late 2023 or early 2024, we're now in territory where refinancing could provide meaningful savings. The general rule of thumb is that refinancing makes sense when you can reduce your rate by at least 0.75% to 1%, enough to offset closing costs within a reasonable timeframe.

The Fed's third rate cut of 2025 is a positive development for the housing market, but it's not a game-changer. More importantly, the Fed's projection of just one cut in 2026 signals that we're entering a new phase—one where rates stabilize rather than continue falling dramatically.

For buyers, this means the time to act may be now rather than waiting for significantly lower rates that may not materialize. For sellers, pricing realistically and understanding that buyers are working with higher borrowing costs will be key to a successful transaction.

The truth is, real estate decisions should never be based solely on interest rates. Your personal circumstances, long-term goals, and local market conditions matter far more than trying to time the Fed perfectly. I've seen people build tremendous wealth buying in "high rate" environments, and I've seen people miss opportunities waiting for perfect conditions that never came.

What I know for certain is this. Homeownership remains one of the most reliable wealth-building tools available to Americans. Yes, the path looks different than it did during the pandemic era of ultra-low rates, but the destination—financial security and the pride of owning your own home—remains as valuable as ever.

The Fed has spoken, the projections are clear, and now it's time to make informed decisions based on reality rather than wishful thinking. Whether rates are at 6%, 7%, or someday back at 4%, the fundamentals of real estate success remain unchanged. Buy wisely, finance smartly, and think long-term.

References: Lane, J. (2025, December 10). Fed cuts rates for 3rd time in 2025, but might cut just once next year. Inman.

Price cuts fell slightly in April 2026 as buyer demand rebounds. See what this means for Orange County buyers and sellers right now.

U.S. home prices rose 2.4% in April 2026, the biggest gain in 13 months. Here's what buyers and sellers in Orange County need to know now.

The U.S. housing market still favors buyers, but the gap is shrinking. Here's what April 2026 data means for Orange County.

Pending home sales hit a nearly 4-year high as mortgage rates dip, inventory grows, and spring buyers finally return to the market.

Inventory is up, purchase apps are surging, and spring is finally delivering. Here's what the latest housing data means for buyers and sellers.

NAR's Yun cuts his 2026 sales forecast from 14% to 4%. Here's what slower growth means for buyers, sellers, and the OC market.

Monthly housing payments rose for the first time in 6 months as mortgage rates and home prices climb amid market uncertainty.

Mortgage rates climbed to 6.38% the week of March 27. Here's what rising rates, shifting inventory, and market uncertainty mean for buyers and sellers.

Mortgage rates hit a 3-month high, monthly payments climb, and buyers pause. Here's what it means for you in Orange County.

Let's find a time that suits you best to chat about your goals, show you how we work, and figure out how we can help you the most

Get In Touch With Lisa

Broker Associate

949-877-7087

124 Tustin Ave Suite 200, Newport Beach, CA 92663