How To Sell a Home With Negative Equity

Lisa Mailhot | June 9, 2025

Buyers

Lisa Mailhot | June 9, 2025

Buyers

Disclaimer: This blog is for informational purposes only and may reference third-party sources, including quotes or data used verbatim with proper credit. All efforts are made to ensure originality and avoid plagiarism. Readers should verify details independently and consult a licensed professional before making real estate decisions.

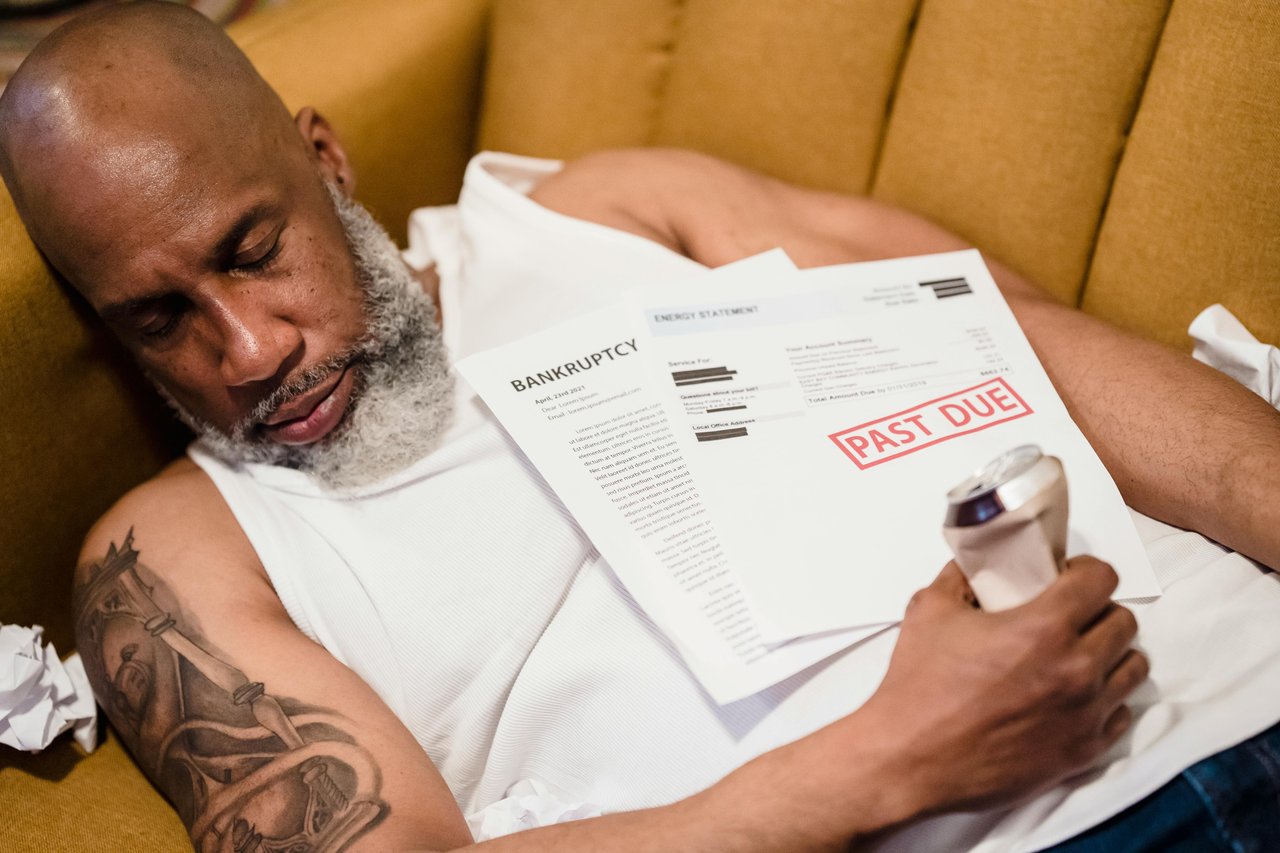

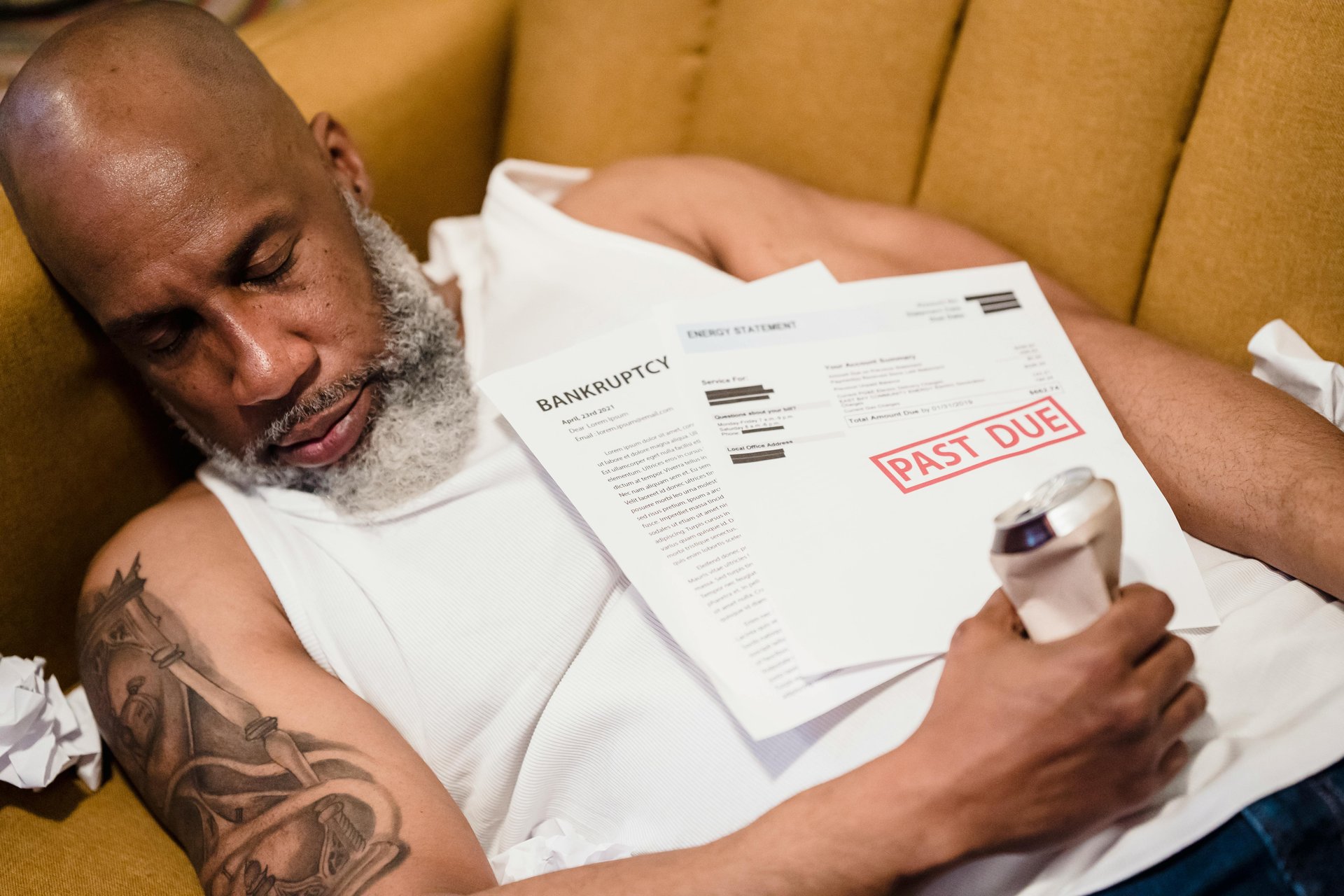

Being underwater—or having a negative equity mortgage—means you owe more on your home loan than your property is currently worth. "In other words, if you were to sell your house today, you wouldn’t bring in enough money to pay off your mortgage balance in full." This situation limits your ability to sell, refinance, or even move, creating serious financial stress for homeowners.

Negative equity can creep up unexpectedly, often due to market shifts or financing terms. The most common causes include:

Buying at or near peak prices: If the housing market cools after you buy, your home's value might drop—sometimes dramatically.

Low down payments: Minimal upfront equity makes it easy to slide underwater with even a small price dip.

High or variable interest rates: Balloon payments or adjustable-rate mortgages can spike your monthly bills and stall principal payoff.

Deferred maintenance or market decline: "If your home has fallen into disrepair or your neighborhood is seeing higher vacancies or job losses," your home’s value can drop fast.

Say you bought a home for $400,000 two years ago with just a 5% down payment. Your mortgage began at around $380,000. Fast forward to today—market shifts have dropped your home’s value to $350,000, and you still owe $370,000. You’re now $20,000 underwater, even though you've been making payments.

While negative equity can happen anywhere, some areas are harder hit than others. "Louisiana led with 11.3% of mortgaged homes seriously underwater," followed by Wyoming, Kentucky, Mississippi, and Oklahoma. Experts point to population declines, job losses, and shifts away from fossil fuel economies as major contributors to falling property values in these areas.

Selling at a loss isn’t easy—but sometimes, it’s the most practical move. Consider selling if:

You can’t afford your mortgage: "Holding out for future home appreciation might not be realistic." Escaping a burdensome mortgage can protect your financial health.

You can't rent it out: If local rental income won’t cover your mortgage or landlord duties aren’t manageable, selling might be smarter.

You need to relocate or face hardship: Divorce, illness, or a job transfer can make waiting for the market to rebound unrealistic.

Your lender approves a short sale: This lets you sell for less than you owe—with potential debt forgiveness—avoiding foreclosure.

Waiting could worsen your situation: "Weigh the risks of waiting against the potential benefits of taking action now."

Every decision has trade-offs. Here's what to consider:

Pros

Frees you from an unaffordable mortgage

Lets you relocate or downsize

May prevent foreclosure with a proactive plan

Cons

You might need to pay the difference out of pocket

It could affect your credit score

You might miss out if the market rebounds later

"Look for a real estate agent experienced in short sales or distressed properties." These professionals know how to price your home right, negotiate with lenders, and avoid legal pitfalls. Real estate attorneys can help protect your rights, especially in judicial foreclosure states.

Don’t wait until you're out of options—contact your lender’s loss mitigation department early, and consider speaking with a HUD-approved housing counselor for free expert advice.

Selling a home when you're underwater isn't just about making the best of a tough situation—it's about reclaiming your financial freedom. At Whitestone Real Estate, we help Orange County homeowners navigate challenges like these every day. Whether you're facing hardship, relocating, or just need to break free from an unaffordable mortgage, let's talk about your options. Reach out today and let’s find your path forward—because your future shouldn’t be tied to a house you can’t afford.

Reference: Suh, E. (2025, June 6). Trapped in a Home You Can’t Afford? Here’s How To Sell With Negative Equity. Realtor.com.

Harvard's 2026 housing report reveals deep affordability struggles nationwide. Here's what it means for Orange County buyers and sellers.

Mortgage rates hover in the mid-6% range this June. Here's what buyers and sellers in Orange County need to know right now.

Home delistings hit near-record highs in April 2026. Learn what's driving sellers to pull listings and what it means for Orange County buyers and sellers.

Homeowners insurance premiums are climbing fast. Learn what's driving costs up and what it means for buyers and sellers in today's market.

Pending home sales drop for the second week as mortgage rates hit a 10-month high. Here's what it means for buyers and sellers today.

Housing affordability improved for 7 straight months. Learn what falling income requirements mean for buyers and sellers in Orange County and beyond.

Price cuts fell slightly in April 2026 as buyer demand rebounds. See what this means for Orange County buyers and sellers right now.

U.S. home prices rose 2.4% in April 2026, the biggest gain in 13 months. Here's what buyers and sellers in Orange County need to know now.

The U.S. housing market still favors buyers, but the gap is shrinking. Here's what April 2026 data means for Orange County.

Let's find a time that suits you best to chat about your goals, show you how we work, and figure out how we can help you the most

Get In Touch With Lisa

Broker Associate

949-877-7087

124 Tustin Ave Suite 200, Newport Beach, CA 92663