Understanding the Current Foreclosure Numbers: A Far Cry from the 2008 Crisis

Lisa Mailhot | July 24, 2023

Buyers

Lisa Mailhot | July 24, 2023

Buyers

If you've been following recent news, you may have seen headlines about an increase in foreclosures in today's housing market. Understandably, this might leave you feeling uncertain, especially if you're considering buying a home. However, it's crucial to look at the context behind these reports to grasp the reality of the situation.

According to a recent report from ATTOM, foreclosure filings have gone up by 2% compared to the previous quarter and 8% compared to last year. While media attention is drawing focus on this increase, reporting solely on the numbers might generate unnecessary worry about a potential market crash. In reality, while foreclosures are on the rise, it does not indicate a foreclosure crisis like what occurred in the past.

We should examine the most recent data with its context to understand how it contrasts with previous years.

Over the past few years, foreclosure rates have reached historic lows. This is primarily due to the implementation of the forbearance program and various relief options in 2020 and 2021, which assisted millions of homeowners in retaining their homes during a challenging period. Simultaneously, the appreciation of home values allowed many homeowners who might have otherwise faced foreclosure to utilize their home equity and opt to sell their properties instead. Looking ahead, equity will remain a significant factor in preventing people from falling into foreclosure.

With the expiration of the government's moratorium, an anticipated increase in foreclosures occurred. However, it's essential to note that this rise in foreclosures does not necessarily indicate trouble for the housing market. As stated by Clare Trapasso, Executive News Editor at Realtor.com:

“Many of these foreclosures would have occurred during the pandemic, but were put off due to federal, state, and local foreclosure moratoriums designed to keep people in their homes . . . Real estate experts have stressed that this isn’t a repeat of the Great Recession. It’s not that scores of homeowners suddenly can’t afford their mortgage payments. Rather, many lenders are now catching up. The foreclosures would have happened during the pandemic if moratoriums hadn’t halted the proceedings.”

Bankrate, in a recent article, also provides an explanation:

“In the years after the housing crash, millions of foreclosures flooded the housing market, depressing prices. That’s not the case now. Most homeowners have a comfortable equity cushion in their homes. Lenders weren’t filing default notices during the height of the pandemic, pushing foreclosures to record lows in 2020. And while there has been a slight uptick in foreclosures since then, it’s nothing like it was.”

Essentially, there won't be an abrupt surge of foreclosures. Instead, the increase is partly attributed to the previously explained delayed activity and partly influenced by economic conditions.

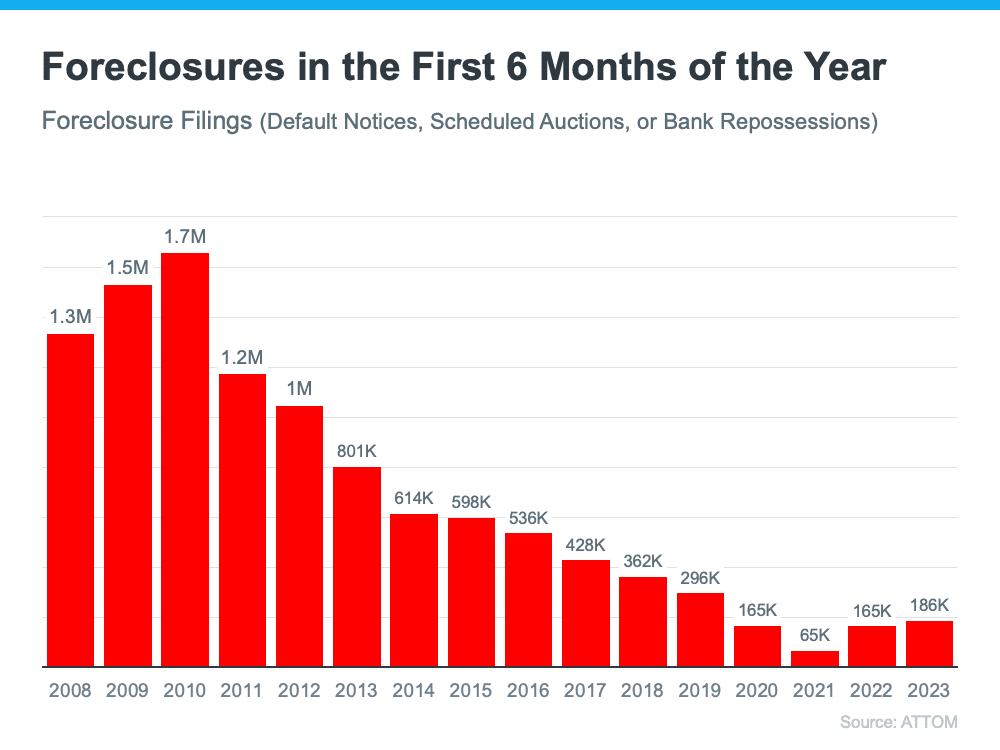

To better illustrate the significant difference between the current situation and the housing crash, refer to the graph below. It presents foreclosure filing data for the first half of each year since 2008, demonstrating that foreclosure activity has consistently remained lower after the crash.

Despite the increase in foreclosures, it is evident that the current foreclosure activity is incomparable to the levels experienced during the housing market crash. Presently, foreclosures are significantly lower than the peak numbers recorded back then.

This can be attributed, in part, to the fact that today's buyers are more qualified and less prone to defaulting on their loans.

It is crucial to contextualize the data at present. Although the housing market is witnessing a predictable rise in foreclosures, it is far from reaching the crisis levels witnessed during the housing bubble burst. Consequently, there is no reason to anticipate a crash in home prices.

Fannie Mae and Freddie Mac's new condo underwriting rules could slow approvals and raise costs. Here's what Orange County buyers and sellers need to know.

A new federal housing law cuts red tape and boosts construction. Here is what it means for Orange County buyers, sellers, and investors.

Homebuyer affordability dropped for a fifth month in a row. Here's what it means for Orange County buyers and sellers and how to plan your next move.

New Redfin data reveals weather beats affordability as the top reason Americans relocate, and Orange County has exactly what movers are chasing.

Pending home sales rose as mortgage rates briefly dipped. Here's what this summer housing market shift means for Orange County buyers and sellers.

Fed Governor Waller wants less forward guidance on rates. Here's what that means for Orange County buyers and sellers trying to time the market.

A new Redfin survey shows most homeowners feel their home reflects who they are. Here's what it means for Orange County buyers.

Harvard's 2026 housing report reveals deep affordability struggles nationwide. Here's what it means for Orange County buyers and sellers.

Mortgage rates hover in the mid-6% range this June. Here's what buyers and sellers in Orange County need to know right now.

Let's find a time that suits you best to chat about your goals, show you how we work, and figure out how we can help you the most

Get In Touch With Lisa

Broker Associate

949-877-7087

124 Tustin Ave Suite 200, Newport Beach, CA 92663