Mortgage Rate Trends: A Historical Perspective and Future Possibilities

Lisa Mailhot | September 6, 2023

Buyers

Lisa Mailhot | September 6, 2023

Buyers

If you're planning to purchase a home this year, you're likely closely monitoring mortgage rates. These rates play a pivotal role in determining your home loan's affordability, and in today's challenging market, it's prudent to examine how mortgage rates compare historically and their potential trajectory. Furthermore, delving into their correlation with inflation can offer valuable insights into their future direction.

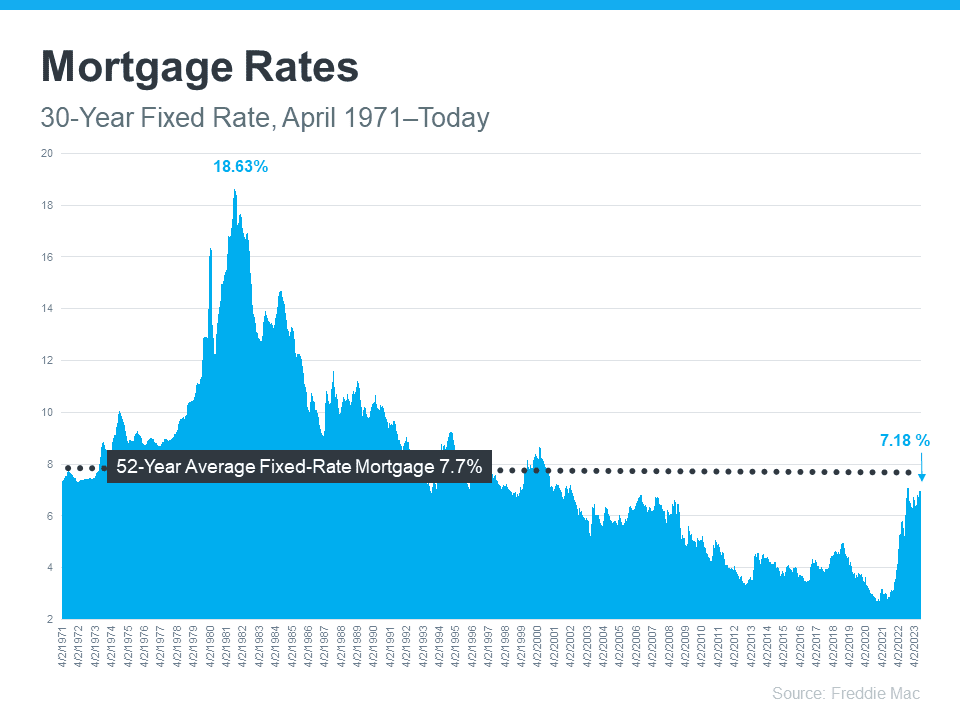

Since April 1971, Freddie Mac has diligently tracked the 30-year fixed mortgage rate. Weekly, they release their findings in the Primary Mortgage Market Survey, which consolidates mortgage application data from lenders nationwide (as depicted in the graph below):

Examining the graph's right side reveals a notable uptick in mortgage rates since the beginning of the past year. Despite this increase, today's rates remain below the 52-year average. While this historical perspective offers valuable context, prospective buyers have grown accustomed to mortgage rates ranging between 3% and 5%, a range they have held for the past 15 years.

This point is significant because it elucidates why recent rate increases might feel surprising, despite them being relatively close to the long-term average. Although many buyers have adapted to these elevated rates over the past year, a slightly lower rate would be warmly welcomed. To gauge whether this is a realistic prospect, it's imperative to assess the inflationary landscape.

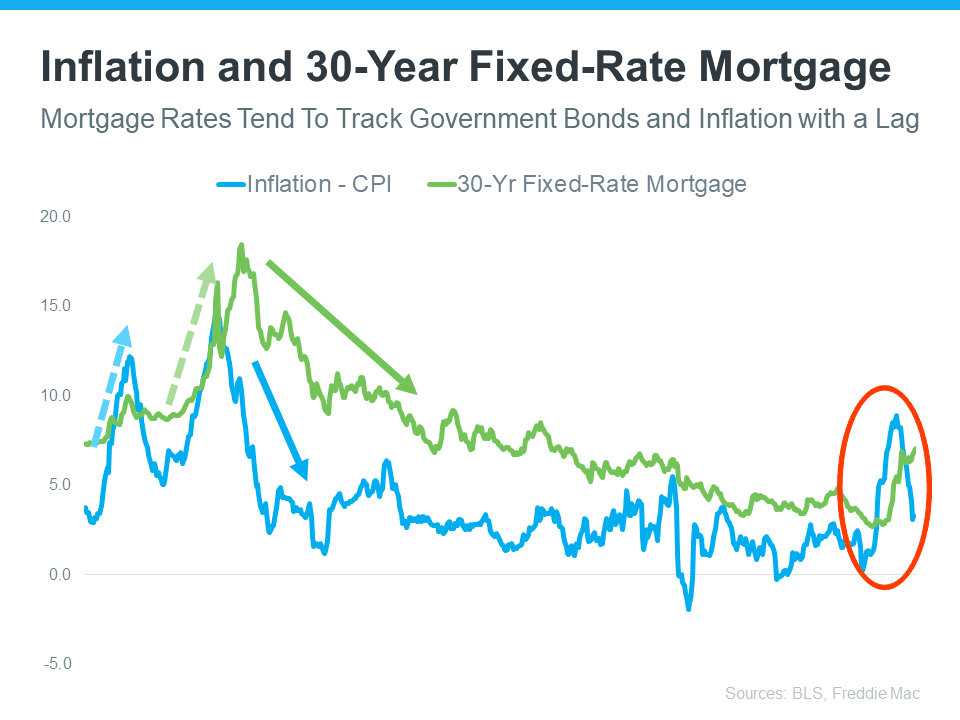

Since early 2022, the Federal Reserve has been diligently working to curb inflation. This is noteworthy because, historically, there exists a correlation between inflation and mortgage rates (consult the graph below):

This graph unveils a rather dependable connection between inflation and mortgage rates. Turning attention to the left side of the graph, it's evident that whenever inflation experiences significant fluctuations (highlighted in blue), mortgage rates subsequently follow suit (highlighted in green).

The circled section of the graph highlights the recent spike in inflation, closely trailed by a corresponding increase in mortgage rates. As inflation has somewhat stabilized this year, mortgage rates have yet to mirror this trend.

This suggests that, based on historical patterns, the market anticipates mortgage rates aligning with inflation and eventually decreasing. While accurately predicting the exact trajectory of mortgage rates is challenging, the moderation of inflation implies that lower mortgage rates in the near future would align with a well-established historical pattern.

To gain insights into the potential direction of mortgage rates, it's advantageous to analyze their historical trajectory. A clear correlation between inflation and mortgage rates exists, and if this historical relationship holds true, the recent reduction in inflation may bode well for the future of mortgage rates and your aspirations of homeownership.

Pending home sales rose as mortgage rates briefly dipped. Here's what this summer housing market shift means for Orange County buyers and sellers.

Fed Governor Waller wants less forward guidance on rates. Here's what that means for Orange County buyers and sellers trying to time the market.

A new Redfin survey shows most homeowners feel their home reflects who they are. Here's what it means for Orange County buyers.

Harvard's 2026 housing report reveals deep affordability struggles nationwide. Here's what it means for Orange County buyers and sellers.

Mortgage rates hover in the mid-6% range this June. Here's what buyers and sellers in Orange County need to know right now.

Home delistings hit near-record highs in April 2026. Learn what's driving sellers to pull listings and what it means for Orange County buyers and sellers.

Homeowners insurance premiums are climbing fast. Learn what's driving costs up and what it means for buyers and sellers in today's market.

Pending home sales drop for the second week as mortgage rates hit a 10-month high. Here's what it means for buyers and sellers today.

Housing affordability improved for 7 straight months. Learn what falling income requirements mean for buyers and sellers in Orange County and beyond.

Let's find a time that suits you best to chat about your goals, show you how we work, and figure out how we can help you the most

Get In Touch With Lisa

Broker Associate

949-877-7087

124 Tustin Ave Suite 200, Newport Beach, CA 92663