The Impending Crash that Isn't: Decoding Today's Housing Inventory

Lisa Mailhot | September 27, 2023

Buyers

Lisa Mailhot | September 27, 2023

Buyers

Remember the housing crisis of 2008? Even if you weren't a homeowner then, the specter of that crash might still linger. But here's the good news: the current real estate landscape is vastly different from what it was in 2008.

One crucial distinction is the scarcity of homes for sale. Unlike in 2008, the market is grappling with undersupply, not oversupply. For a market crash to occur, there would need to be an excess of houses on the market. However, the data doesn't support such a scenario.

Housing supply originates from three primary sources:

Now, let's delve deeper into the current housing inventory to grasp why this situation differs significantly from what transpired in 2008:

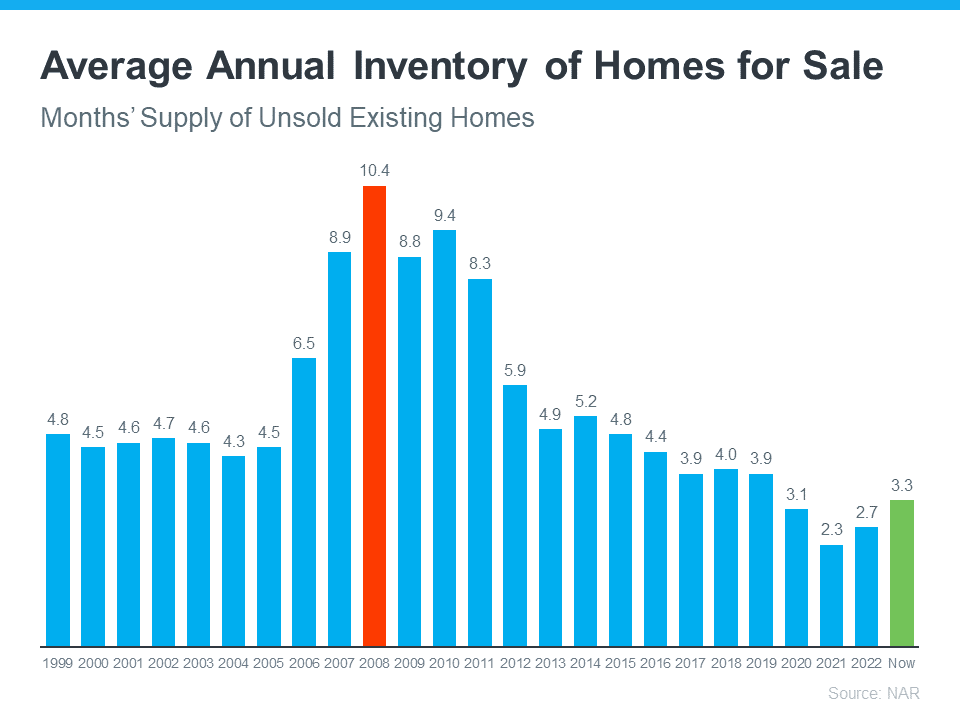

While housing supply has increased compared to the previous year, it remains relatively low. The current month's supply is below the normal levels. A glance at the graph below reveals a stark contrast between the latest data (in green) and 2008 (in red), with only about one-third of the available inventory today.

What does this signify? Simply put, there are not enough homes on the market to cause a significant decline in home values. To recreate the 2008 scenario, we would need a substantial increase in home sellers and a scarcity of buyers, which is not the case today.

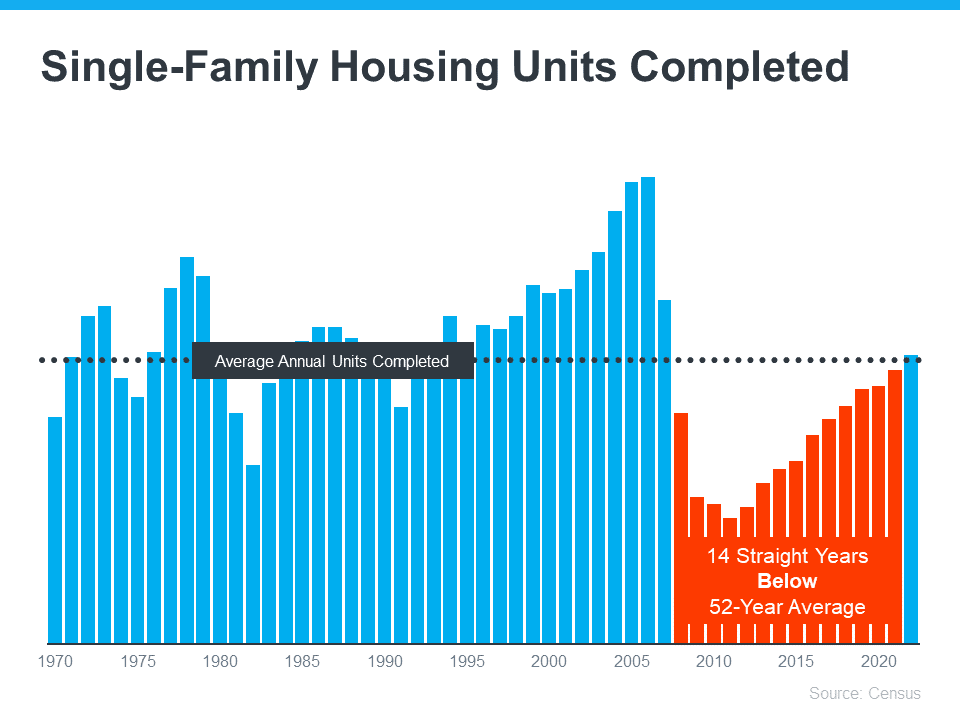

There is much talk about the construction of new homes, leading to questions about potential overbuilding. The graph below illustrates the number of new homes built over the past 52 years:

The 14-year period of underbuilding (depicted in red) is a major factor contributing to today's low inventory. Builders have not been constructing enough homes for quite some time, resulting in a significant supply shortfall.

While the final blue bar on the graph shows an increase that is on track to meet the long-term average, it will not suddenly lead to an oversupply. The gap to be filled is simply too substantial, and builders are cautious about not repeating the overbuilding mistakes of the past.

The last source of inventory is distressed properties, such as foreclosures and short sales. During the housing crisis, an influx of foreclosures occurred due to lenient lending standards that allowed many people to secure loans they couldn't truly afford.

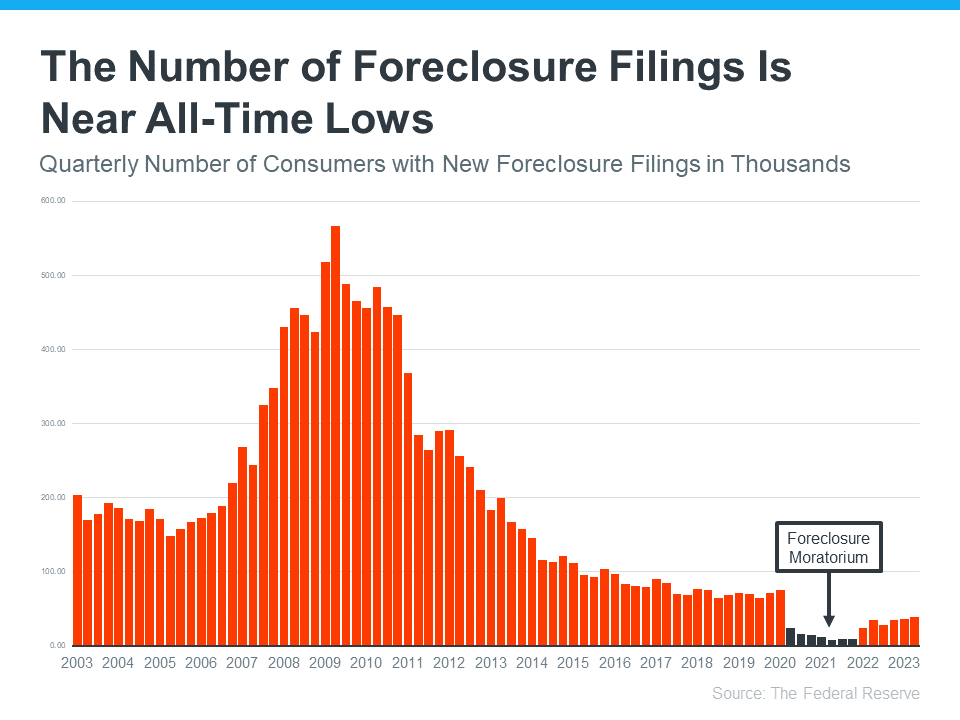

Today, lending standards are much stricter, resulting in more qualified buyers and significantly fewer foreclosures. The graph below, based on data from the Federal Reserve, demonstrates the changes since the housing crash:

This graph illustrates that as lending standards tightened and buyers became more qualified, the number of foreclosures decreased. In 2020 and 2021, a combination of foreclosure moratoriums and forbearance programs helped prevent a repeat of the foreclosure wave seen in 2008.

The forbearance program was a game changer, offering homeowners options like loan deferrals and modifications that were not available before. Data on the program's success shows that four out of every five homeowners emerging from forbearance have either paid in full or worked out a repayment plan to avoid foreclosure. These factors are key reasons why we won't see a surge of foreclosures hitting the market.

The current inventory levels are far from the threshold required for significant price drops and a housing market crash. According to Bankrate, this situation is unlikely to change in the near future, especially with robust buyer demand:

“This ongoing lack of inventory explains why many buyers still have little choice but to bid up prices. And it also indicates that the supply-and-demand equation simply won’t allow a price crash in the near future.”

The housing market does not possess the surplus homes necessary for a repeat of the 2008 housing crisis, and there is no evidence to suggest that this situation will change in the near future. Housing inventory data indicates that a crash is not on the horizon.

The 2026 summer housing market has slowed nationwide, giving buyers more time and leverage. Here's what it means for Orange County movers.

Fannie Mae and Freddie Mac's new condo underwriting rules could slow approvals and raise costs. Here's what Orange County buyers and sellers need to know.

A new federal housing law cuts red tape and boosts construction. Here is what it means for Orange County buyers, sellers, and investors.

Homebuyer affordability dropped for a fifth month in a row. Here's what it means for Orange County buyers and sellers and how to plan your next move.

New Redfin data reveals weather beats affordability as the top reason Americans relocate, and Orange County has exactly what movers are chasing.

Pending home sales rose as mortgage rates briefly dipped. Here's what this summer housing market shift means for Orange County buyers and sellers.

Fed Governor Waller wants less forward guidance on rates. Here's what that means for Orange County buyers and sellers trying to time the market.

A new Redfin survey shows most homeowners feel their home reflects who they are. Here's what it means for Orange County buyers.

Harvard's 2026 housing report reveals deep affordability struggles nationwide. Here's what it means for Orange County buyers and sellers.

Let's find a time that suits you best to chat about your goals, show you how we work, and figure out how we can help you the most

Get In Touch With Lisa

Broker Associate

949-877-7087

124 Tustin Ave Suite 200, Newport Beach, CA 92663